To continue reading the rest of this article, please log in.

Create free account to get unlimited news articles and more!

Australia and New Zealand Banking Group (ANZ), the Commonwealth Bank of Australia (CBA), National Australia Bank (NAB), and Westpac Banking Corporation (Westpac) have all announced interest rate rises on their loan products of 25 basis points (bps).

Following on from yesterday’s (3 May) decision by the Reserve Bank of Australia (RBA) to raise interest rates from their record-low levels (starting an increasing rate cycle for the first time in nearly 12 years), the major banks have been quick to pass on the full amount of home loan borrowers.

It is expected that other lenders will follow suit and raise their rates in due course, with Suncorp having already announced it would raise variable mortgage rates by 25 basis points, and hike 12-month term deposit rates by 0.40 per cent, from 18 May.

ANZ

Standard variable interest rates for Australian home and residential investment loans at ANZ will increase by 0.25 per cent per annum (p.a.), bringing the index rate to 4.64 per cent p.a. for those making principal and interest (P&I) repayments and 5.19 per cent p.a. for those on interest-only (IO) repayments.

It estimates the 25-basis-point change will increase monthly repayments by $57 on an average home loan of $450,000 for an owner-occupier paying P&I.

The bank said it would also increase the Progress Saver bonus interest rate by 0.25 per cent p.a, meaning ANZ customers with a Progress Saver account will get a total rate of 0.40 per cent inclusive of the bonus rate.

All rate changes are effective from 13 May 2022.

Speaking of the decision to change mortgage rates, ANZ’s group executive Australia retail, Maile Carnegie, said: “In making this decision we considered various factors including the change in the official cash rate, along with the impact on our customers and our business performance.

“While this change will impact customers in different ways, home loan customers are generally well placed to manage rising rates with around 70 per cent of accounts ahead on repayments – many of them by two years or more. Household and business deposits are also at record highs.

“However, we know some people are doing it tough and we encourage any ANZ home loan customers facing difficulty to contact us so we can work through a range of support options we have available.”

She continued: “It has been a difficult environment for savers in recent years with record low rates, so this increase we have announced... will help them reach their savings goals faster. "

CBA

For CBA home loan customers, standard variable rates for owner-occupiers will increase 25 bps to 4.80 per cent p.a. for those on P&I repayments and to 5.29 per cent p.a. for those on IO repayments.

Investors will see P&I repayments rise by the same amount, to 5.38 per cent p.a., while investors making IO repayments will see rates rise to 5.64 per cent p.a.

The new home loan variable interest rates will take effect on 20 May 2022.

The group executive, retail banking, Angus Sullivan said: “This is an important time to support customers as some may not have experienced an interest rate increase since they took out their loans.

“We are here to help customers who have loans and are considering how repayments might change. Some options available to help our customers manage repayments include fixing or splitting loans or setting up an offset account.”

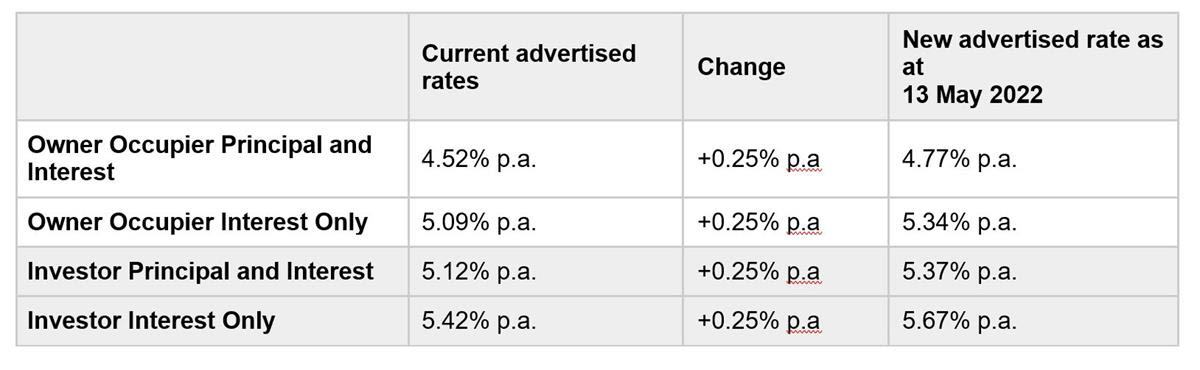

NAB

As well as hiking rates for mortgagors by 25 bps, NAB has also confirmed that it will increase interest rates on savings accounts, which have been at record lows.

The standard variable home loan will increase by 0.25 per cent to 4.77 per cent p.a. and the reward saver bonus interest rate will increase by 0.25 per cent.

The new loan rates are as follows:

According to the bank, a NAB owner-occupier customer paying principal and interest on a 30-year $400,000 mortgage would see repayments rise by an additional $57 a month (for a NAB Choice package variable rate of 3.67 per cent p.a.)

NAB’s new consumer savings and home loan rates will be effective on 13 May 2022.

NAB group executive personal banking Rachel Slade commented: “Supporting customers through the change is a priority for NAB. Interest rates have been very low for a long time – it has been 11 years since the official cash rate in Australia last increased and we know this will be a new experience for some customers.

“We will look after our customers if they find changes to interest rates challenging.”

Ms Slade highlighted that the bank has online resources to help borrowers access information about how to manage changes to their home loans and has “also made it easy for customers to switch from variable to fixed rates” in the NAB app.

She continued: “While we have 930,000 home loan customers, the historic low interest rates have been difficult for our savings and deposit customers, including more than 1.3 million customers with a reward saver account.

“We want to support them as interest rates rise again.”

Westpac

Like NAB, Westpac is also passing the full 25 bps rise to both mortgagors and savers.

Both new and existing home loan customers will be subject to the rate rise on home loans, with the standard variable rate rising to 4.73 per cent p.a. for those on P&I repayments.

Westpac will also increase interest rates for selected consumer deposit accounts Westpac Life and Westpac 55+ and Retired by 0.25 per cent p.a.

Westpac’s new rates will take effect from 17 May 2022.

“We have made the decision to increase our standard variable rate for home loan and selected consumer deposit customers following [the] increase to the official cash rate,” Chris de Bruin, Westpac’s chief executive of consumer and business banking, said.

“We know many of our customers were able to build-up their savings during the pandemic and 70 per cent of home loan customers are ahead on their repayments, helping put them in a better position to withstand an interest rate rise.

“We are also increasing interest rates on some of our most popular products for savers, which will provide some relief following a period of record low interest rates.

“We know that some home loan customers may still experience difficulty and we encourage these customers to call us as soon as possible, so our specialist customer teams can work with them to tailor a financial solution.”

All four major banks have outlined that any customers experiencing hardship or seeking help to manage repayments should contact their bank.

However, given that more than two-thirds of all home loans are now written by mortgage brokers, it is expected that brokers will also be very busy helping their clients understand the new environment and help borrowers consider their ability to repay.